From savings to investment - Part 2

From savings to investment - Part 2

How much, in what, how, diversification, portfolio and other stories...

If you don’t know who you are, this is an expensive place to find out.

George Goodman

In the last article we discussed the transition from savings to investment.

The step from having money set aside to avoid being dependent and to be able to respond to unforeseen events to putting money into production.

Producing more money. Of course.

We were saying that you should only invest the surplus savings that you are able to assume that you can lose completely and still sleep peacefully.

Or at least sleep.

If you can't assume that with certain money, keep it in the bank.

- OK.

I have a certain amount of time saved.

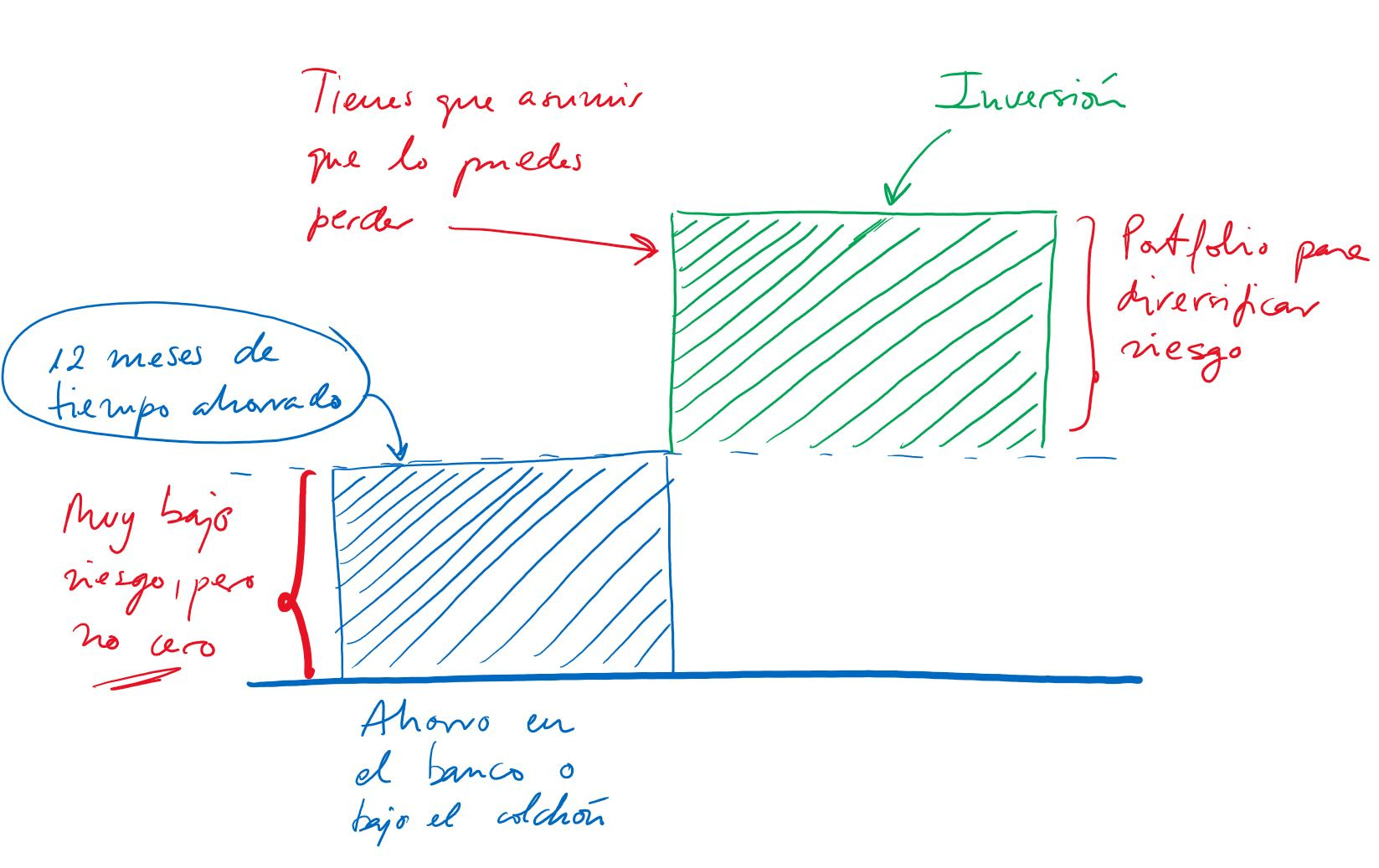

I have already applied your advice: with my current standard of living I can be 12 months earning zero income and living. So I have saved a year's worth of non-dependency.

What can I do with what goes over that savings threshold that I am comfortable with?

Okay, let's talk about some best practices on how to put that money to work.

Diversify, portfolio and risk: investment first

When you put your money to produce you have to take into account one fundamental thing: you enter a higher level of risk than the one you were in before.

We have already explained that not even the bank has zero risk, but this is another thing, this happens to have levels of risk notoriously superior to having the money in a bank.

Once that is assumed: not all risks were created equal.

The ideal, over time, is that you can build a portfolio, an investment portfolio containing different assets chosen in such a way that they provide you:

Diversification: not putting all your eggs in one basket. Now let's take a closer look

Different levels of risk: not having everything at the same level of risk.

I am going to tell you what an aspirational portfolio of this type can look like so that you can start thinking about whether you are interested in building it.

Remember that my first recommendation is that you get advice from experts. I am not one. In fact, I consult with them.

Your money when you have savings and you have a surplus that you can invest will look like this if you follow the advice of La Forja:

A cushion of time in the form of money in the bank (or under your bed) and a surplus to be invested with other levels of risk.

Obviously, not everything is to put fear, but I do want to be quite cautious with this topic because there are plenty of ads about getting rich investing in Amazon, about stock market courses or about turbo-trading-intraday-robo-advisor-red-bull with which you will earn your first million in a month.

What interests us at La Forja is something else, it is that you forge a toolbox as solid as possible and designed for the long term.

I know nothing about intraday trading, my thing is fire, the gloves and the hammer.

Blow by blow to build it up.

There are people with a more sophisticated style, but this is mine. And I like it.

Call me classic or ignorant. That's at your judgment.

Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.

Paul Samuelson

If it's not all about to put fear, then you're also doing this looking for something positive. That something is the capital gains that your investments can generate.

That's why I recommend you make them: so that your money generates more money.

Risk and the ability to generate capital gains are inseparable twins, so write this down:

If you can expect to make 15% on an investment, you can also lose 15%.

From the little I know about investing, this is one of the solid rock laws I do know.

Anyone who tells you otherwise, at the very least, be suspicious and discuss it with your financial advisor.

The linearity between risk and capital gain is admirable because of how easy it is to understand.

It is also very tricky: there is no way to get around it.

- With this, can I expect to earn 15% annually?

- And to lose 15% as well...

- And with this 30%?

- And to lose it too...

- I don't want so much risk, I'll be happy with 5%, what the hell, I'll be happy with 1%....

- So, you accept to be able to lose 5% or 1%...

As you can see, it has no trick.

But that is not a bad thing, it is a good thing, because it is predictable.

If you are investing in an asset that can earn you 15% you know perfectly well that you can lose 15% just as easily and that allows you to build your investment portfolio knowing the levels of risk you run with each asset and creating the most suitable mix for you.

In most places where personal finance is discussed, the emphasis is on financial assets and in particular on stock market investment.

I'm going to try to open up the field a little more, because there is more under the sun, even if there is little talk about it.

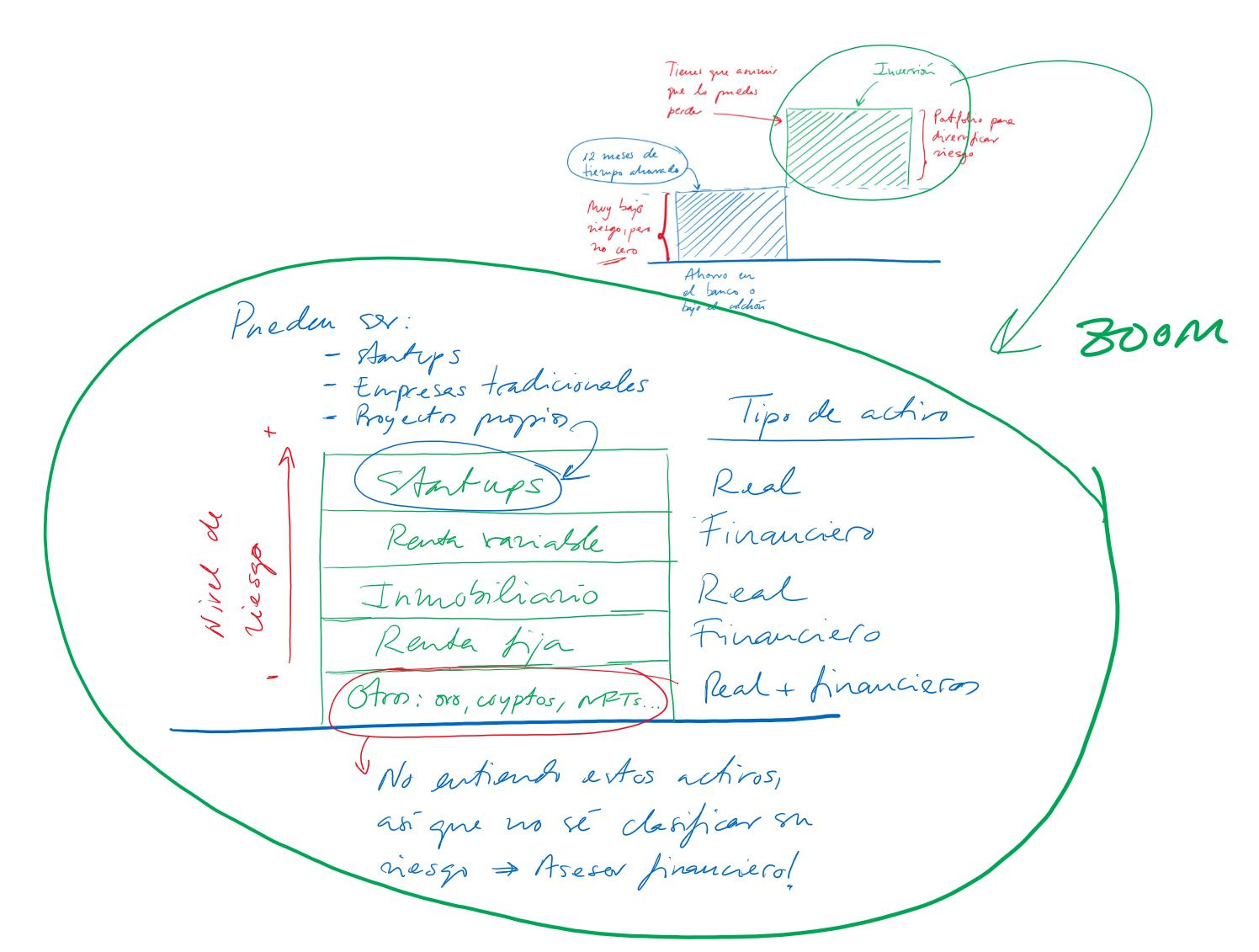

Let's look at a possible mix that you could build:

In the image, we have zoomed in on the investment part of the previous graph and shown its detail.

Disclaimer: everything from here on is a simplification, and a gross one at that, but I don't want to exceed myself with what I don't know and it is not the objective of La Forja. I simplify and go to the concepts.

In the image we see several things:

In your investment portfolio you have to take into account the risk of the assets that compose it so that you feel comfortable with the portfolio you build.

This is personal and non-transferable.

I recommend that you mix levels of risk and types of assets, so that if some fall you can expect that others will not. All your eggs in the same basket...

Notice how I have ordered the risk levels in the portfolio in the image, from lowest to highest:

Fixed income: this can be country debt, public debt or corporate debt, private debt.

It is called fixed because you know from the moment you invest the return you are going to get (if nothing goes wrong).

Fixed income is a world in itself, but let's simplify by saying that it is one of the assets with the lowest risk (depending on the country/company you choose).

As it is one of the lowest risk assets it is also one of the lowest return assets.

The relationship between risk and capital gains is a fucking one, as we have already said.

Real estate: investing in bricks, in a flat, in a garage.

This is a type of investment also of little risk in general terms and compared to the alternatives (here everything is of much or little compared to what), but some already know big scares with real estate markets.

Many more people are familiar with this type of investment than with the others, so we explain it less.

Equities: any investment in which we do not know its return, which can be anything, including 0%.

What is most commonly identified with equities are shares of listed companies, but not only that, also commodities, currencies, etc., but I take them out of here for simplicity.

In addition to the shares of listed companies (on any stock exchange in the world), this also includes the well-known investment funds and any financial instrument that has shares (or equity assets) underneath.

It is really not worth entering here without studying it and discussing it with your advisor. This is a world in itself and La Forja is not about this, but about discovering that it exists.

What we are interested in knowing about equities is that they can generate better returns, better capital gains than other assets like the above.

It can do that.

It can also make us lose much more than the other assets.

Startups: new companies, typically innovative and with a strong technological base (although not always).

This is an asset that is not usually mentioned much in sites that talk about personal finance, but since I am close to that world, I include it because I think they are very interesting investments.

The risk of this type of investment pulverizes everything detailed so far. That is why investing in Startups is called Venture Capital. Its name is not misleading.

A series of founding partners have an idea and create a company to carry it out. That can end up being Google or it can go bankrupt after 18 months.

Anything is possible. Most likely it will go bankrupt, followed by it surviving in a zombie state (chickens in for chickens out) and very rarely do they work.

When they work, capital gains range from moderate and achievable with another type of investment to wild, where we no longer speak of profitability percentages, but of multipliers: multiplying the investment by 4, by 10 or by 20.

Multiplying by 4 is equivalent to 400% profitability. To give you an example.

So you see that the possible returns are so radical that the other assets cannot even come close to them and, in turn, the risk is just as radical.

That a part of your portfolio in Startups can be interesting if your risk level tolerates it.

In addition to Startups, which are a very particular type of investment in real economy (not financial), I have also included in the image that you can invest in companies.

Yes, you can. From your friend's bar because you think it is going to work and needs capital to using your money to launch an own project.

Few people do this, but it can be done.

Others: cryptocurrencies (cryptos), gold and commodities in general (which I have put here and not in equities because for me they are exotic investments that I do not know), NFT and anything else that you could make public.

I don't know anything about this, I just know they exist.

In fact I have a friend trying to educate me on cryptos and me not having time to do it.

That is why I have put them and I have not classified their risk (they are out of the scale, not in the lowest step).

With this I want to exemplify that I neither understand those assets, nor have criteria to invest in them nor have I been advised to do so (because life has a limit) and, therefore, I do not touch them.

Does this mean that they are not good?

No, it means that since I do not understand them, nor their level of risk, I do not touch them.

That is the example I want to convey to you.

For some people NFTs are things they do not understand and do not touch them, for others a Fintech startup is just as mysterious and they will never invest in it because they do not understand what it is, nor its sector, nor its business model, nor anything else. Therefore, he is right not to touch it.

There seems to be an unwritten rule on Wall Street: If you don’t understand it, then put your life savings into it.

Peter Lynch

In the next article we will go a little deeper into Startup investing because there are curious people asking about that world and we will also go a little into what we can expect from investing in long term equities with compound interest.

- But... Let's see, I'm saving some money, with effort. Is this what you're telling me for big investors?

- What do you mean?

- Do you must have a lot of money or can any average citizen aspire to it?

- The headline is that any citizen can, more than you think. What happens is that you have to know that you can.

Going out to burn capital by eating out is better known, but there are other options with the money.

We will see it in the next article.

José Fortes - La Forja.

josefortes@substack.com

If you like La Forja, subscribe and share it.